Introduction:

Geographical proximity and strategic positioning explain Tunisia’s close relationships and intense economic and trade relations with the countries of the European Union. This so-called “natural” exchange zone has gradually turned into an “official” zone following the various trade agreements established since 1969[1]. The latest agreement, approved in November 2012, aims to further integrate the Tunisian economy into the EU through the establishment of the Deep and Comprehensive Free Trade Agreement (DCFTA).

At the heart of the European Neighborhood Policy and the Association Agreement, DCFTA is part of the so-called second-generation partnerships or WTO+. Beyond dismantling tariffs on industrial products and establishing concessions in exchange for agricultural products, this partnership envisages a liberalization of all sectors and an alignment of economic and legal regulations.

Several sectors[2] are preparing for negotiations under this privileged partnership. Some of them have already provoked strong controversy within Tunisian civil society since the beginning of the negotiations in October 2015. Several voices have risen to oppose the agreement and to consider it “colonialist” as it symbolizes a new level of subordination to Western powers[3]. Yet, many experts believe that this is the ideal opportunity to help the country successfully integrate into the global economy. Hence, weighing the pros and cons of adhering to this partnership is a rather difficult task.

This policy brief firstly shows the potential economic, political and social risks that joining DCFTA poses for Tunisia secondly but also demonstrates how, if certain assets are developed, this partnership could be an opportunity to implement major reforms.

Opposition to the DCFTA: Perceptions and facts

Popular backlash to Regional Trade Agreements (RTAs) is not unique to Tunisia as, in recent years, support for these agreements has declined. As a result, civil society discontent has blocked new partnerships, such as the TTIP[4] between the EU and the USA or CETA[5] between the EU and Canada, and has led to questioning historical agreements, such as the United Kingdom’s departure from the EU (Brexit). Moreover, conflicts between governments and political oppositions over the ratification of an agreement have even led in some cases to a reversal of power and the outbreak of civil wars, such as in Ukraine in 2013[6].

In Tunisia, calls to block the DCFTA are often justified by the risks the agreement would pose to three areas in particular: guarantee of intellectual property rights, access to public markets, and exchange of agricultural products. Indeed, the extension of medication patents beyond the 20-year limit, set by the WTO, raises concerns amongst professionals in the pharmaceutical industry. This EU proposal is considered a threat to the production of generic (non branded) drugs that cover 70% of the needs of Tunisians. The resulting price increase would exacerbate public health problems in the country.

Article 2 of the chapter on public procurement, entitled “Non-discrimination”[7], allows Tunisian and EU companies to take part in public tenders on an equal footing which presents a triad of threats. Firstly, there’s a risk that small and medium-sized enterprises (SMEs) would be stripped of the favors granted by the public authorities[8]. Secondly, there is a risk of losing the possibility of gaining public contracts, which are often used as a means of applying certain development strategies and achieving several socio-economic objectives. And finally, this poses a risk to national sovereignty if these markets involve areas of state security.

Furthermore, the major concern is with the agricultural sector, which, according to a IACE (Arab Institute of Business Leaders) survey in 2017[9], has the lowest perception index and is the most against the DCFTA. Under this agreement, both parties declare their willingness to offer significant liberalization on agricultural, fishery, and processed agricultural products, with some exceptions on each side. This is known as the “negative list” approach, which excludes sensitive products that require specific treatment from liberalization. This approach is widely contested s, because an almost complete opening of Tunisian agriculture sector, in its current state, could cause economic, social, and environmental risks because there is vast inequality, in terms of competitiveness, between the two sides.

These inequalities are caused mainly by the climatic conditions and the technological gap but especially because farmers in EU states benefit from Common Agricultural Policy (CAP) subsidies. Agricultural liberalization under these conditions will certainly contribute to the disappearance of small farms operating mainly in the field of cereals, meat, and milk (70% of holdings do not exceed 10 hectares)[10]. The other threat is to the reorientation of agricultural activity from strategic products to export-oriented products, which are generally very intensive in terms of water consumption. In addition to the ecological risks, these major changes will undoubtedly pose a threat to food sovereignty. Tunisia is also called upon to progressively bring its sanitary and phytosanitary (SPS) regulations into line with the EU standards. These new standards are very difficult for Tunisian farmers to meet, given their limited access to information, technical expertise, and sources of funding.

The risks of the DCFTA for the Tunisian economy are thus very real. A bad negotiation of the agreement could accelerate the degradation of public health services, could ruin small farmers, may accentuate the desertification of the rural areas. The agreement could even threaten the Tunisia’s sovereignty of the state, especially if the arbitration system, originally proposed by the EU, is included. However, it must be acknowledged that the Tunisian economy in its current state would not benefit from this particular agreement or all others types of partnerships in general. An archaic, unmodernized agricultural sector that consists of fragmented and weather-dependent land can never compete with a modern and subsidized agriculture system. The fragile public health sector will not be able to handle the production of generic drugs. Nepotism and corruption that taint tender processes will likely persist despite the introduction of a degree of competition and transparency in the award of public contracts. Therefore, it is especially urgent to launch major reforms, long-awaited since the events of 2011.

The implications of a successful DCFTA for Tunisia?

There are economic, political, social, and environmental obstacles to the implementation of the DCFTA but this is no reason to abandon the negotiations altogether. Since the agreement is in a very early stage, there is still time to seize the opportunity and prepare counter-proposals. Beyond risks and constraints, the Tunisian economy has several assets. Knowing how to develop them could enable it to establish a “win-win” partnership with the EU.

Promising potential for better integration into the Global Value Chains (GVCs)

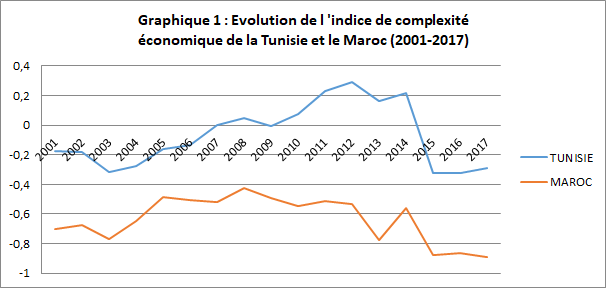

Tunisia has always been an export-oriented economy, however, this openness has failed to record sufficient growth rates to absorb both an ever-growing and increasingly structural unemployment, especially in recent years. The country has witnessed a sharp increase in the diversification and sophistication of its exported products, especially in the mechanical, electronic, and pharmaceutical sectors. Compared to several other economies in the region, Tunisia has a higher level of economic complexity, including Morocco, its main competitor. (Figure 1). However, the country is expected to further improve its position in GVCs, to achieve the levels of growth needed for significant job creation, and consequently allowing the absorption of the ever-increasing levels of unemployment. Based on several empirical studies, Rodrik (2006) and Hausmann et al. (2007)[11] argue that economies that specialize in highly sophisticated products grow faster than those that specialize in a more basic range of products. The authors conclude that better integration into GVCs would therefore offer opportunities for structural transformation, especially for developing countries.

In addition to sound industrial policy and continued investment in skills development, the harmonization of regulations and the easing of customs procedures under the DCFTA would undoubtedly contribute to the creation of a favorable business climate for better attractiveness of FDI (Foreign direct investment) and a better positioning of Tunisia within the GVCs.

A promising service sector, especially in non-traditional products

In Tunisia, the balance of services has mostly been positive in a constant manner, which, with factor income/s, attenuated the deficit in the trade balance which reached record levels in recent years. Despite their importance, these traditional services generate rather uncertain revenues and remain highly dependent on the security conditions of the country. Moreover, trade in this sector, unlike industrial products, lacks diversification, both in terms of exported services and the markets for which they are intended. Indeed, in 2017, travel and transport accounted for 70% of total exports, of which 60% is destined for only three markets, namely France, Italy, and Germany (Charts 2 and 3).

However, Tunisia has great potential in other services, such as computer services and medical care, which account for only a small share of exports but have risen sharply in recent years. These services recorded a growth of 34% and 50% respectively between 2017 and 2018[12]. The DCFTA’s opening of these promising sectors would allow more innovation and improved product quality for both domestic and foreign consumers. This sector can be a driving force in for economic development. Several studies even argue that the opening of European markets to Tunisian companies under the DCFTA may allow Tunisia to retain and benefit from the young skilled workforce that is currently seeking to leave the country[13].

The development of the services sector in Tunisia and the improvement of its competitiveness largely depend on two key factors. On the one hand, the modernization of logistics and transport, especially the maritime one, is considered as cornerstones of international trade. On the other hand, the introduction of more flexibility in the mobility of service providers and the facilitation of visa issuance. Negotiations on this subject are not part of the DCFTA but are dealt with separately in the framework of the Mobility Partnership, which must necessarily be synchronized with the DCFTA.

A participatory approach with increased civil society and the private sector involvement

Unlike previous agreements, DCFTA benefits from a relatively large communication campaign and an increasingly wide-ranging consultation with civil society. Although the efforts made are often considered insufficient, especially concerning the transparency of the proposals on the Tunisian side, there has, so far, been significant effort to communicate the terms and details of the deal. [14]. The major problem with regional agreements is that they are often presented in complicated legal jargon, added to the fact that their socioeconomic effects are very difficult to assess. Indeed, they generally involve large short-term costs concentrated on very distinct social groups, while the gains will only be dispersed over the long-term overall economic agents. This vagueness fuels the fear and mistrust of DCFTA, which will present opportunities for some and threats for others. Thus, good communication and awareness-raising will help identify risks and the required solutions. The discussion with the harmed parties about the possibilities of their compensation and the accompanying measures would make it easier to accept much-feared costly reforms.

Nevertheless, the controversy for or against the DCFTA, and the momentum created during the discussions animated by the civil society, can only be a good exercise for the young democracy. However, the debates must now take a more technical direction by raising awareness among professionals in the different concerned sectors.

Conclusion

Although the current context, national and international, is not conducive to the immediate pursuit of the DCFTA negotiations, but a total blockage would be a serious mistake. Blocking this agreement would lead to blocking major reforms in Tunisia. Indeed, the DCFTA should not be considered objective in itself. It must be part of a more global strategy and vision that considers the future of Tunisia’s agriculture sector, the type of comparative advantage that can be achieved, and what support SMEs need to improve their positioning in global value chains.

Tunisia must make the best use of the two fundamental principles of this agreement, i.e. progressivity and asymmetry, to set its priorities and allow the DCFTA to be an accelerator of reforms. It should be noted, however, that beyond risks and economic benefits, adherence to a regional agreement remains primarily a political issue. Political stability can undoubtedly provide a climate of trust that can make reforms accept and accelerate. On the other hand, it is very difficult to lead big projects amidst a situation of tension. Opposing the DCFTA is an argument widely used in populist election campaigns. At the same time, it should be remembered that, when negotiations continue, where appropriate, mistrust is still a matter of urgency. Indeed, if theoretically and according to the principle of progressiveness, Tunisia is free to decide the “when” and “what” release, it is necessary to ensure that these decisions do not meet the interests of some lobbies. This is where the important role of civil society, which remains the main safeguard for preventing such abuses, manifests itself.

Recommendations

To make the DCFTA successful for Tunisia, we should:

- Insert the DCFTA into a global vision of the Tunisian economy and consider it as a catalyst for major reforms, which should enhance existing competitive advantages and boost promising sectors.

- Improve the quality of logistics such as transport infrastructure and efficiency of customs clearance processes to make Tunisia more attractive for FDI and further integration into GVCs, thus strengthening Tunisia’s negotiating power.

- Improve communication with aggrieved parties, such as small farmers, about adjustment costs and accompanying measures provided for in the agreement.

- Adopt a good negotiation position that allows for the best use of the principles of asymmetry and progressivity and a choice of the “positive list” rather than “negative list” approach.

- Significant technical and financial assistance, which must necessarily be conditioned by the state of progress of the reforms.

- Increase the number of meetings with representatives of the signatory countries of the DCFTA with the EU, in particular Ukraine, Moldova and Georgia in order to share experiences and increase the capacities of Tunisian negotiators.

- Increase transparency regarding the counter-proposals from the Tunisian side which are not revealed to the public, unlike the European proposals which are published and each time updated on the committee’s website.

- Give privileged place to civil society and regional level discussions in the debate on the DCFTA, to prevent the agreement from serving the interests of particular lobbies.

[1] First Trade Agreement signed in March 1969 between the European Economic Community of Six and Tunisia. [2] An explanatory sheet for each domain is available at http://www.aleca.tn/decouvrir-l-aleca/domaines-de-l-accord/[3] Constitution on 24 May 2019 of a national collective, “Block DCFTA”, led by the Tunisian General Labor Union (UGTT ), the Tunisian Union of Agriculture and Fisheries (UTAP), and several other associations and organizations.[4] Transatlantic Trade and Investment Partnership. [5] Comprehensive Economic Trade Agreement. [6] Adarov, A and Havlik, P,. Benefits and Costs of DCFTA: Evaluation of the Impact on Georgia, Moldova and Ukraine, WP (2016). Available at https://wiiw.ac.at/benefits-and-costs-of-dcfta-evaluation-of-the-impact-on-georgia-moldova-and-ukraine-dlp-4111.pdf [7] https://trade.ec.europa.eu/doclib/docs/2016/april/tradoc_154484.pdf [8] As the reservation of a percentage within the limit of 20% of the value of works contracts, studies and supply of goods and services to companies employing between 6 and 49 employees (Decree No. 2008-561 of 4 March 2008).[9] IACE, «Indice de perception de l’ALECA en Tunisie», available at http://www.iace.tn/wp-content/uploads/2017/06/INDICE_PERCEPTION_ALECA_edition_2_2017_NBA.pdf [10] FTDES, «Perceptions de l’Accord de Libre Echange Complet et Approfondi (ALECA) : Etude des attentes et conséquences économiques et sociales en Tunisie », Octobre 2018, p : 31. [11] Hausmann R, Hidalgo C, Klinger B, & Barabási A, “The product space conditions the development of nations Science”, Jul 2007, 317(5837), pp. 482-487. Rodrik D, “What’s So Special about China’s exports?”, China & World Economy, 2006, 14 (5), pp. 1-19. [12] Data from the 2018 Central Bank Report.[13] Solidar Report (2018) p.10. [14] Tunisian Ministry of Commerce and Handicrafts website to disseminate information and interact with civil society. available at http://www.tunisie-ue-aleca.tn/